STUDENT LOANS

Student loans are offered at low interest rates and can be repaid over an extended period. The Financial Aid Office will verify your eligibility based on the information you provide on your Free Application for Federal Student Aid (FAFSA), the first step in applying for any financial aid.

You may qualify for student loans. They are a serious financial obligation and must be repaid. Be sure to look for other forms of financial aid that don’t have to be paid back, like grants or scholarships first. The academy encourages you to review all information about loans before deciding to borrow and to borrow only what you need.

Loan Availability

- Federal Direct Loans

- Federal Direct Loans, from the William D. Ford Federal Direct Loan Program, are low-interest loans for eligible students to help cover the cost of higher education.

- Federal Direct Subsidized Loans

- Federal Direct Subsidized Loans are offered to students with financial need. You are not charged interest while you’re in school at least half-time, during grace periods, or deferment periods If you receive a Federal Direct Subsidized Loan that is first disbursed between July 1, 2012 and July 1, 2014, you will be responsible for paying any interest that accrues during your grace period If you choose not to pay the interest that accrues during your grace period, the interest will be added to your principal balance

- Federal Direct Unsubsidized Loans

- Federal Direct Unsubsidized Loans are NOT based on financial need. Interest is charged from the time the loan is disbursed until it is paid in full You can pay the interest while you are in school and during grace periods and deferment or forbearance periods, or you can allow it to accrue and be capitalized (added to the principal amount of your loan) If you choose not to pay the interest as it accrues, this will increase the total amount you must repay because you will be charged interest on a higher principal amount Loan eligibility is determined by completing the FAFSA. Loan limits are determined by grade level and prior borrowed amounts. There is a small loan fee charged prior to funds being received at the academy. Interest is charged on Direct loans. Before your loan money is disbursed, you may cancel all or part of your loan at any time. After your loan is disbursed, you may cancel all or part of the loan within 14 days of receiving the loan.

- Federal Direct PLUS Loan

- To be considered for a Federal Direct PLUS Loan: The student must complete a FAFSA (Free Application for Federal Student Assistance) The parent must obtain an FSA ID Students and parents must be a U.S. Citizen or eligible non-citizen Students and parents must not be in default on a federal education loan or owe an overpayment on an educational grant Student must be enrolled at least half-time (minimum of six credits) Student must attend classes and maintain Satisfactory Academic Progress Applicant cannot have an adverse credit history. A credit check is required for approval. Applicant must complete the Federal Direct Parent PLUS Loan Certification Form Applicant must complete the Federal Direct PLUS Master Promissory Note

- Private Loans

- A private loan is a last resort and is not recommended. Be sure all other federal loan options have been exhausted before taking out a private loan for school. The academy requires that U.S. Citizens and/or permanent residents first complete a FAFSA and apply for a Federal Direct Stafford Loan before applying for private loans. Federal Direct Stafford Loans have lower interest rates and offer borrowers better benefits than private loans. Students are urged to speak with a Financial Assistance Counselor for guidance when considering their loan options. Private student loans are not guaranteed by the federal government, require a credit check and often a co-signer. Loan terms and conditions vary significantly by lender. Carefully consider your financial needs and then select the loan product that best meets both your individual situation and your financial need. When researching private loans, you should pay close attention to the borrower benefits, fees, interest rates and repayment options. To calculate the interest, lenders typically use the LIBOR Rate average, Prime Rate, or the 91-Day T-bill. Reasons to Consider a Private Loan Private student loans provide a choice when circumstances necessitate one. Consider a private student loan if: You have reached your Federal Direct Stafford Loan borrowing limit. You have expenses that your financial assistance does not cover. You have a balance due from a previous term.

Applying for a Loan

- Federal Direct Loans

- The first step in applying for any financial aid at the academy, including grants, loans, scholarships and student employment, is to complete the FAFSA (Free Application for Federal Student Aid). Information for First-Time Loan Borrowers If you are a first-time borrower at the academy, you will be required to: Accept, reduce or decline the loans offered to you based on your eligibility. If your enrollment drops below half-time before loans are disbursed to your student account, you may not receive payment. After the funds are disbursed to your student account, the award will not change. Complete Federal Direct Stafford Loan Entrance Counseling at http://www.studentloans.gov, which explains your rights and responsibilities as a loan borrower and is required for all first-time borrowers at the academy. Complete your Direct Loan Master Promissory Note (MPN) at http://www.studentloans.gov, using your FSA ID. The MPN is the legal document in which you promise to repay your loan(s) and any accrued interest and fees to the U.S. Department of Education. It also explains the terms and conditions of your loan(s); for instance, it will include information on how interest is calculated and what deferment and cancellation provision are available to you. These steps must be completed before you can receive your first loan disbursement. First-time, first-year loan borrowers will not receive their first loan disbursement until 30 calendar days after the first day of classes, per federal regulations. However, at the academy we do not disburse loans until 30 calendar days after the first day of classes for all students who attend the school. Your loan will be submitted to the National Student Loan Data System (NSLDS) and will be accessible by guaranty agencies, lenders, and schools determined to be authorized users of the data system.

- Federal Direct PLUS Loan

- The Federal PLUS Loan is not based on financial need; however, the academy requires completion of the FAFSA (Free Application for Federal Student Aid). Complete the Federal Direct Parent Loan for Undergraduate Students (PLUS) form, which is available from the Financial Aid Office. Complete the Federal Direct PLUS Master Promissory Note on http://www.studentloans.gov. This only needs to be completed once while your student attends the academy. If your student attends less than full-time during any term, the Cost of Attendance and financial aid award amounts will be adjusted. This could result in reduction or removal of loans or other financial aid. There is a loan fee charged prior to funds being received at the academy. Interest is charged on PLUS Loans.

Entrance Counseling

If you have not previously received a Direct Loan or Federal Family Education Loan (FFEL), the Federal Government requires you to complete entrance counseling at http://www.studentloans.gov to ensure that you understand the responsibilities and obligations you are assuming.

If you complete your entrance counseling to borrow a loan as an undergraduate student, then the entrance counseling fulfills counseling requirements for Direct Subsidized Loans and Direct Unsubsidized Loans.

Loan Agreement (Master Promissory Note)

The Master Promissory Note (MPN) is a legal document in which you promise to repay your loan(s) and any accrued interest and fees to the U.S. Department of Education. It also explains the terms and conditions of your loan(s). Unless your school does not allow more than one loan to be made under the same MPN, you can borrow additional Direct Loans on a single MPN for up to 10 years. Your school will tell you what loans, if any, you are eligible to receive.

Exit Counseling

If you are graduating, withdrawing, or dropping below half-time, you must complete Student Loan Exit Counseling at http://www.studentloans.gov. Exit counseling provides important information you need to prepare to repay your federal student loan(s).

If you have received a subsidized, unsubsidized or PLUS loan under the Direct Loan Program or the FFEL Program, you must complete exit counseling each time you:

- Drop below half-time enrollment

- Graduate

- Leave School

Note: The FFEL Program ended June 30, 2010 and no new loans have been made under the FFEL Program after that date.

At the end of the exit counseling session, you will be asked for information that will be included as part of your loan records. You must provide the following:

- Names, addresses, e-mail addresses and phone numbers for:

- Your next of kin

- Two references who live in the U.S.

- Your future employer (if known)

To complete Exit Counseling as an undergraduate student, you will need:

- Approximately 20-30 minutes to complete.

- Exit Counseling must be completed in a single session.

- Your FSA ID

- If you are a new user or have forgotten your FSA ID, go to http://fsaid.ed.gov.

- Students must log in using their own FSA ID to complete Exit Counseling. Use of another person’s FSA ID constitutes fraud. Use only your own FSA ID information.

- Name(s) of the school(s) you wish to notify of counseling completion

Loan Repayment

You begin repaying Federal Direct Stafford loans six months after graduation, leaving school, or dropping below half-time enrollment. You must complete federally required Exit Counseling before you graduate from the academy, if you drop below half-time attendance, or withdraw from classes completely. Your academic records will be on hold until this is completed.

- Repayment

- The Department of Education offers Loan Repayment Plans and Calculators and information on loan forgiveness and cancellation. You must repay the full amount of your loan regardless of whether you complete the program or complete within the regular time for completion, are unable to obtain employment upon completion, or are otherwise dissatisfied with or do not receive the educational or other services you purchase from the school. There is no penalty for prepayment.

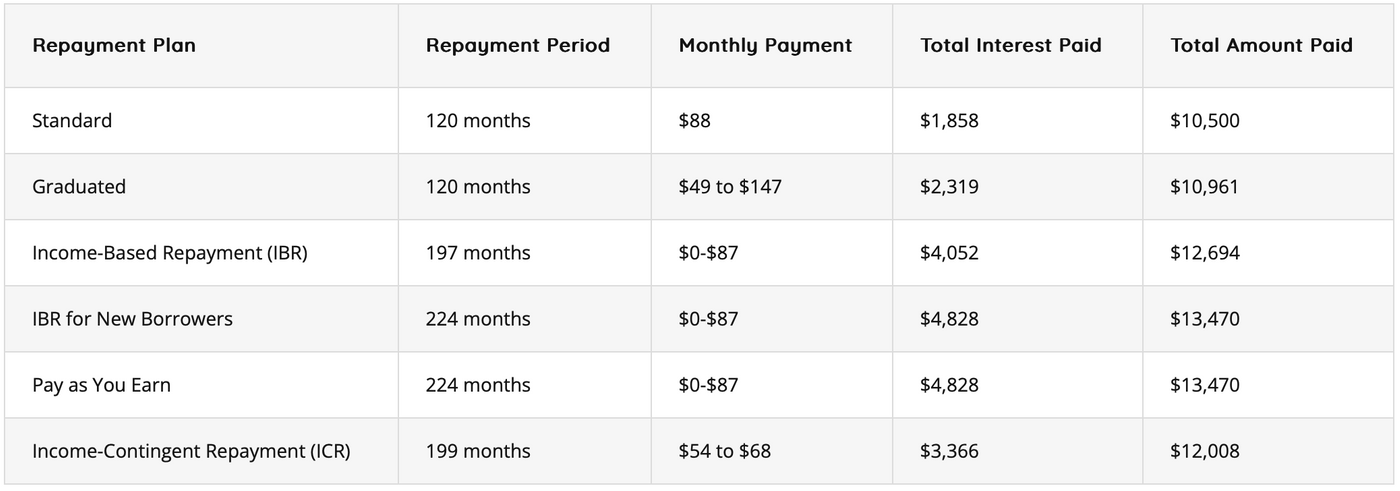

- Sample Loan Repayment Amounts

- Example: $2880 in subsidized plus $5762 in unsubsidized loans with a 4% interest rate; Married Filing Jointly; $30,000 Adjusted Gross Income; family size of 3; living in Florida

Student Loan Services

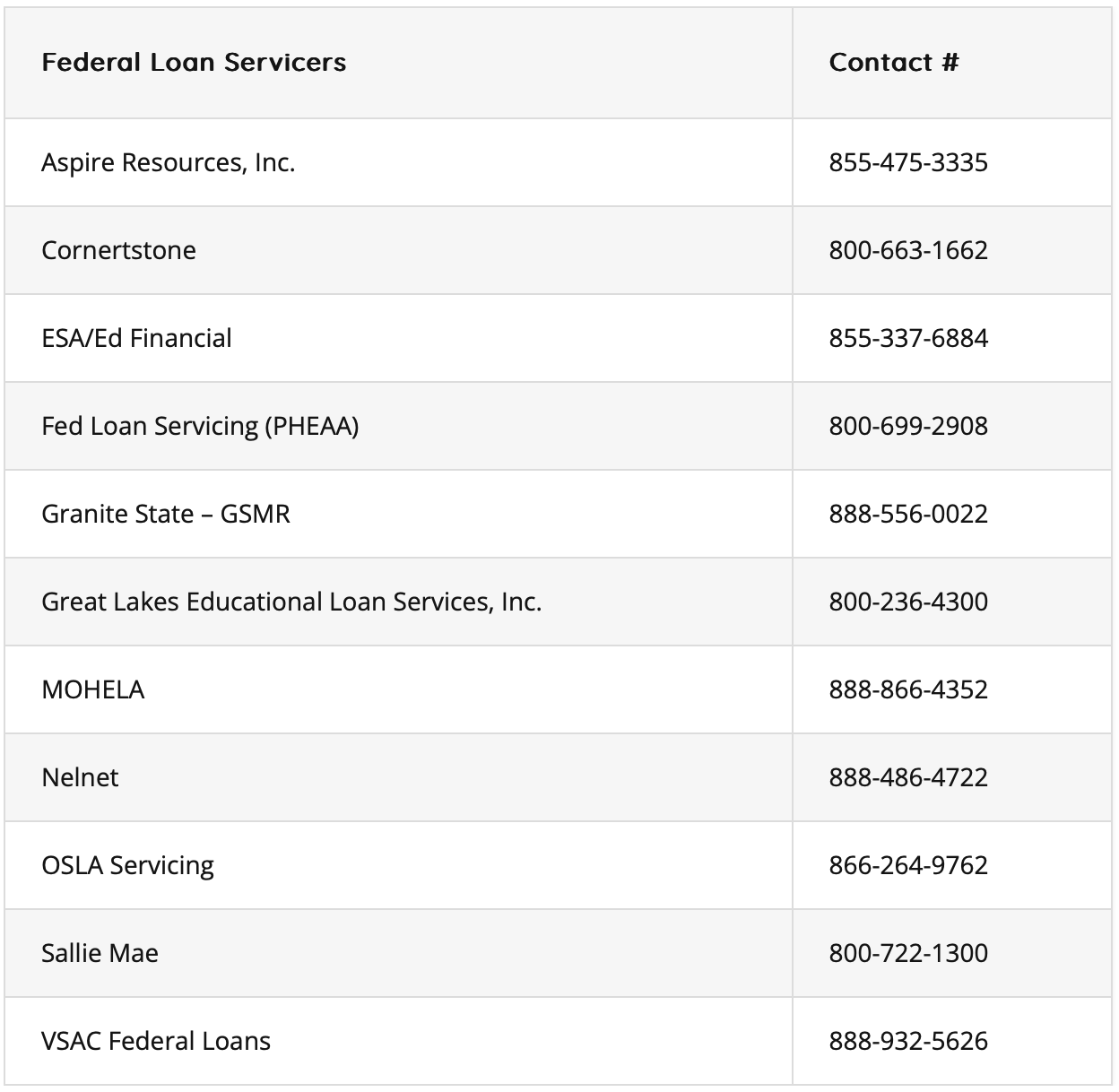

When your loan is due, your federal loan servicer will mail you a payment schedule with your monthly payment of principal and interest, and the unpaid balance for each month it takes to repay your total debt. If they do not contact you, you are still responsible for making payments. Login to Federal Student Aid for find your Federal Loan Servicer.

Federal Student Aid Ombudsman Group

If you’re in a dispute about your federal student loan, contact the Federal Student Aid Ombudsman Group as a last resort. The Ombudsman Group is a neutral, informal, and confidential resource to help resolve disputes about your federal student loans. You may also call 877-557-2575, fax 606-396-4821, or write to FSA Ombudsman Group, P.O. Box 1843, Monticello, KY 42633.

National Student Loan Data System (NSLDS)

With your FSA ID, you can access NSLDS, a national database that contains your financial aid grant and loan history from any school, including the academy. This includes grants, federal Stafford and PLUS loans, whether borrowed directly from the Federal government or a private lender. Private loans are not listed on NSLDS. NSLDS is accessible by guaranty agencies, lenders, and institutions determined to be authorized users of the data system.

Consolidation

The Federal Direct Consolidation Loan Program allows you to combine one or more certain federal student loans and to make one monthly payment to the federal government. There is no charge for consolidation, and repayment plans are offered. The interest rate is fixed for the life of the loan and cannot exceed 8.25 percent.

- Pros & Cons of Loan Consolidation

- PROS Locks in the interest rate Allows the borrower to combine loans from multiple lenders into a single repayment schedule (i.e., one monthly payment) Allows the borrower a longer repayment period, which will reduce the amount of the borrower’s monthly payment Allows a borrower to clear an over-award of Stafford loans or clear a defaulted student loan CONS Locks in the interest rate, for older Stafford loans that have a variable interest rate May increase the total cost of the borrower’s loan, the longer the repayment, the more interest you will pay Borrower may have to forfeit all or a portion of the grace period Borrower may lose certain borrower benefits related to their current loans Certain deferments may be lost; however, borrowers retain their ability to request most major deferments Borrowers who consolidate Perkins Loans lose the deferment subsidy and cancellation eligibility options related to Perkins loans

- Loans that Can Be Consolidated

- Federal Direct Loans and Federal Family Education Loan(s) that are eligible for loan consolidation include: Stafford PLUS SLS Previous Consolidation Loans Perkins Loans Health Professional Student Loans Nursing Student Loans Health Education Assistance Loans (HEAL) Federally Insured Student Loans (FISL) *Alternative loans are not eligible to be included in a Federal Consolidation Loan

Loan Deferment and Forbearance

If you have trouble making your education loan payments, you may qualify for a deferment (a temporary suspension of loan payments for specific situations such as reenrollment in school, unemployment or economic hardship) or a forbearance (a temporary postponement or reduction of payments for a period because you are experiencing financial difficulty).

These periods do not count toward the length of time you have to repay your loan. You cannot get a deferment or forbearance for a loan that is already in default. You must continue making payments on your student loan until you have been notified that a deferment or forbearance has been granted.

To request a deferment or forbearance, contact your individual Federal Loan Servicer. Login to Federal Student Aid to find your Federal Loan Servicer.

- Deferment

- A deferment is a period during which no payments are required, and interest continues to accrue on the unsubsidized portion. Interest does not accrue on the subsidized portion. PLUS, borrowers may defer repayment while the student is enrolled at least half-time. To qualify for a deferment, you must meet at least one of the eligibility requirements listed below, with certain conditions: Be enrolled at least half-time at a postsecondary school Study in an approved graduate fellowship program or in an approved rehabilitation training program for the disabled Be unable to find full-time employment (up to 3 years) Face an economic hardship including Peace Corps Service (up to 3 years) Be on Active Military Duty – If a borrower is called to active duty during a war, other military operation or national emergency and if the borrower was serving on or after Oct. 1, 2007, the borrower qualifies for an additional 180-day period following the demobilization date for the qualifying service.

- Forbearance

- If you temporarily cannot meet your repayment schedule, but you are not eligible for a deferment, your lender might grant you forbearance for a limited and specific period. Interest continues to accrue, and you are responsible to pay it. Generally, your lender can grant forbearance for periods up to 12 months at a time, for a maximum of three years. You will need to provide documentation to the lender to show why you should be granted forbearance. The lender must send you a notice confirming the terms that were agreed to and record them in your file. Receiving a forbearance is not automatic: you must apply for it.

Loan Default

Default is a serious consequence for not repaying your loans. It will occur if you fail to make a payment for 270 days. The school, lender, or agency that holds your loan may all act to recover the money.

Not paying back your student loans can have serious consequences including:

- The lender can require that you repay the entire amount immediately, including all interest, collections, and late payment charges.

- The lender can sue you and can ask the federal government for help in collecting from you.

- The lender can garnish your wages.

- The Internal Revenue Service may withhold your income tax refund and apply it toward your loan repayment.

- You cannot get any additional federal student aid until you make satisfactory arrangements to repay your loan.

- The lender may notify credit bureaus of your default. This may affect your credit rating, which will make it difficult to obtain credit cards, car and/or home loans in the future.

There are several options for repaying your loans if you suffer a financial hardship or other circumstances. In many cases, default can be avoided by submitting a request for a deferment, forbearance, discharge, or cancellation and by providing the required documentation.